If you have supported the country on army or try already offering, you could potentially take advantage of a Va mortgage. The application form allows veterans so you can qualify for a home loan no down payment demands (closing costs nonetheless apply and you may down-payment calculated according to readily available entitlement), preventing the have to expect ages to save sufficient money.

Brand new eligibility rules imply that more folks than you possibly might think you are going to be eligible for good Virtual assistant financing. Besides providing full-date, the fresh federal shield and you can reserves and additionally meet the requirements together with cadets and you can midshipmen from the naval academy. Thriving spouses away from pros plus descendants may take advantage of so it mortgage system.

Financial Insurance coverage

While the Va doesn’t require borrowers to pay private home loan insurance coverage when they have below 20% security, they do enjoys a funding percentage one individuals have to pay. There are exemptions if you suffer from a disability, but if not, which commission could well be ranging from step 1.25% and you may 3.3% of your own amount borrowed based on their downpayment.

Lower settlement costs

Va financing plus reduce the matter you’ll shell out in closing will cost you. There are specific will cost you you to definitely other individuals pays one an effective veteran would not (new 1% will be billed using the term off underwriting or running).

A great deal more choice no charges

You could select often fixed or variable-price mortgage loans over symptoms ranging from ten and 3 decades. Adjustable-rates mortgages will have a period of a reduced fixed attention payday loan Keystone price that would be as long as eight decades.

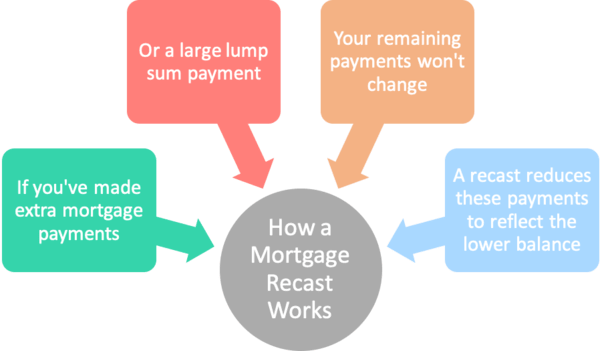

If you decide to pay off their home loan very early, it’s not necessary to value prepayment penalties. Therefore regardless if you are expenses a lump sum to reduce the home loan or increasing your monthly payments, you will not end up being punished to possess doing this.

Second-tier entitlements

With a great Virtual assistant mortgage, you will be in a position to get another household once defaulting into a past financial. Although you can expect to face a great deal more analysis nevertheless fulfill the normal financial obligation-to-money criteria, it could make it easier to recover from financial challenge.

You could be able to qualify for the next Va mortgage for those who have a permanent Change of Station (PCS) or other improvement in family activities.

Being qualified getting an excellent Va loan

Even though you see the experienced conditions, you continue to have to satisfy its debt-to-earnings ratio regulations become acknowledged for a loan. Whenever home loan repayments are included near the top of other expenses, it cannot be more 41% of the borrower’s month-to-month gross income.

There is also guidance on how much discretionary earnings will be left over after paying costs. This provides brand new debtor sufficient money to fund dining, dresses, resources, or any other essentials away from existence, which can be part of the reason why such mortgages feel the reduced pricing regarding default.

Virtual assistant money commonly right for people that maybe not offered otherwise become a wife of someone who has got. If you aren’t an experienced you simply can’t make the most of that it zero deposit requirements bodies system.

If you don’t need to take their zero deposit choice and have now 20% currently conserved, these types of financing is almost certainly not your very best choices. With an effective 20% deposit, you could potentially prevent the money payment necessary for the newest Virtual assistant of the playing with a different type of financial.

This new Va mortgage system lets experts to help you refinance within a lower price by way of the improve refinance choice. But not, should you want to cash out whenever refinancing, you are restricted to ninety% of your own value of the home. This might signify you can get less cash if funding payment is roofed than the other choices.