The credit get you need to pick a house are a the least 620 to help you qualify for a compliant old-fashioned mortgage, though private lenders might require highest results than it.

Debt-to-money ratio

Your debt-to-income proportion (DTI) is the count you pay https://paydayloanalabama.com/gadsden/ with the debts each month divided by your gross monthly money. Like, for many who spend $2,000 thirty days on your own mortgage and you can education loan money and you can you earn $step three,000 thirty day period, your DTI proportion is $2,000 split up because of the $3,000, otherwise 66%.

Once you make an application for a home loan, their potential future homeloan payment might be included in this computation. Getting conforming conventional mortgages, you can even meet the requirements with a whole DTI ratio as much as 50%. But the restrict DTI you can get will depend on the complete financial character, as well as your credit rating and you may down payment count. Their DTI should be no higher than thirty six% to get the finest likelihood of getting accepted.

Deposit

Having compliant funds, minimal deposit you are able to is step three%, though some lenders might need at the very least 5% or ten%. Jumbo fund might require 10% or maybe more, however it varies from financial so you’re able to financial.

For many who set-out below 20% to your a conforming mortgage, you will need to purchase individual financial insurance if you do not come to 20% equity in the home. Which month-to-month cost will be placed into the home loan repayments. You are able to basically shell out ranging from $29 and you will $70 thirty days each $100,000 your use, centered on Freddie Mac.

Paperwork

In the long run, you will need to offer the bank with many monetary papers so you’re able to show you feel the income and come up with your instalments. This normally includes tax statements, W-2s, bank statements, shell out stubs, and.

Conventional mortgage loans vs. almost every other financing brands

You are getting a normal financial from an exclusive lender, instance a lender, a great nonbank mortgage lender, or a card commitment. Regardless of if an authorities institution will not ensure these types of loans, of numerous old-fashioned mortgages are supported by authorities-sponsored people Fannie mae and Freddie Mac computer. The loan could well be marketed to one of those organizations immediately following closure.

By contrast, a government-backed home loan includes insurance policies otherwise guarantees you to a federal company, for instance the Government Housing Government, You Department off Farming, otherwise Institution away from Experts Circumstances, will cover part of the financial in the event your borrower non-payments. This is how those differ from traditional money:

- FHA loans: FHA funds commonly allow for all the way down fico scores than old-fashioned money (right down to five hundred oftentimes), even though they have highest advance payment requirements (at the least step three.5% in place of a normal loan’s step three%). Nevertheless they need home loan insurance rates upfront and over the loan title.

- Va loans:Virtual assistant financing are only for pros, army professionals, as well as their partners. They won’t need an advance payment, but there is an upfront capital payment.

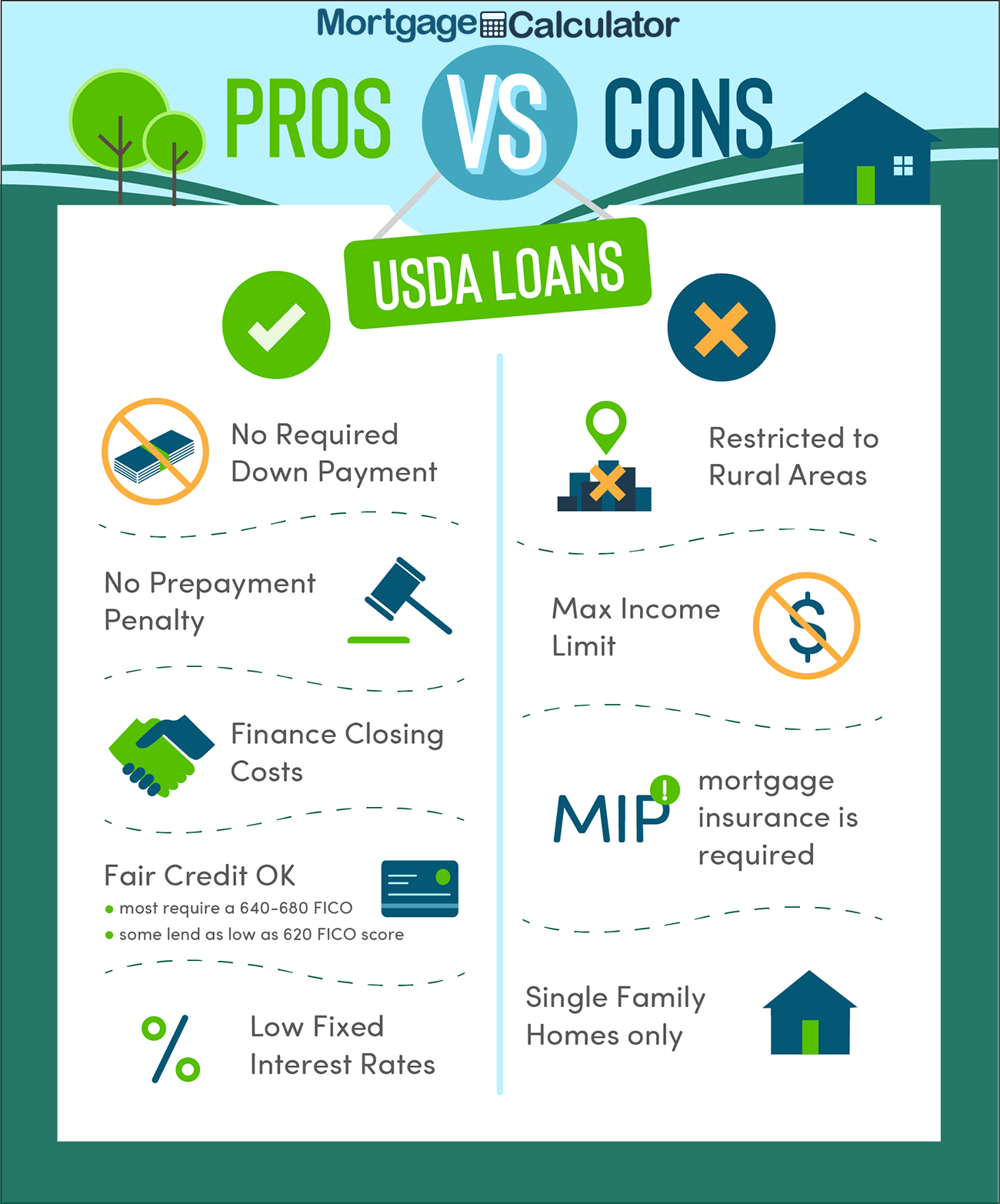

- USDA fund:USDA fund can only just be employed to get property into the eligible outlying places, and you have to have a qualifying reduced so you’re able to reasonable income for your area in order to meet the requirements. Zero downpayment becomes necessary, but there is an initial guarantee percentage.

Ways to get a traditional financial

Compliant, old-fashioned mortgage loans are definitely the most well known mortgage device on the market, so if you’re offered one of those fund, you’re not by yourself. Here is how to locate your own:

Step 1: Look at your borrowing

Pull their borrowing from the bank, and find out just what rating you happen to be working with before you apply for your loan. The better their get, the easier and simpler it could be so you’re able to be considered (together with ideal your interest would be.) If it is towards the lower end, you can make a plan to alter it ahead of filling aside a loan application.